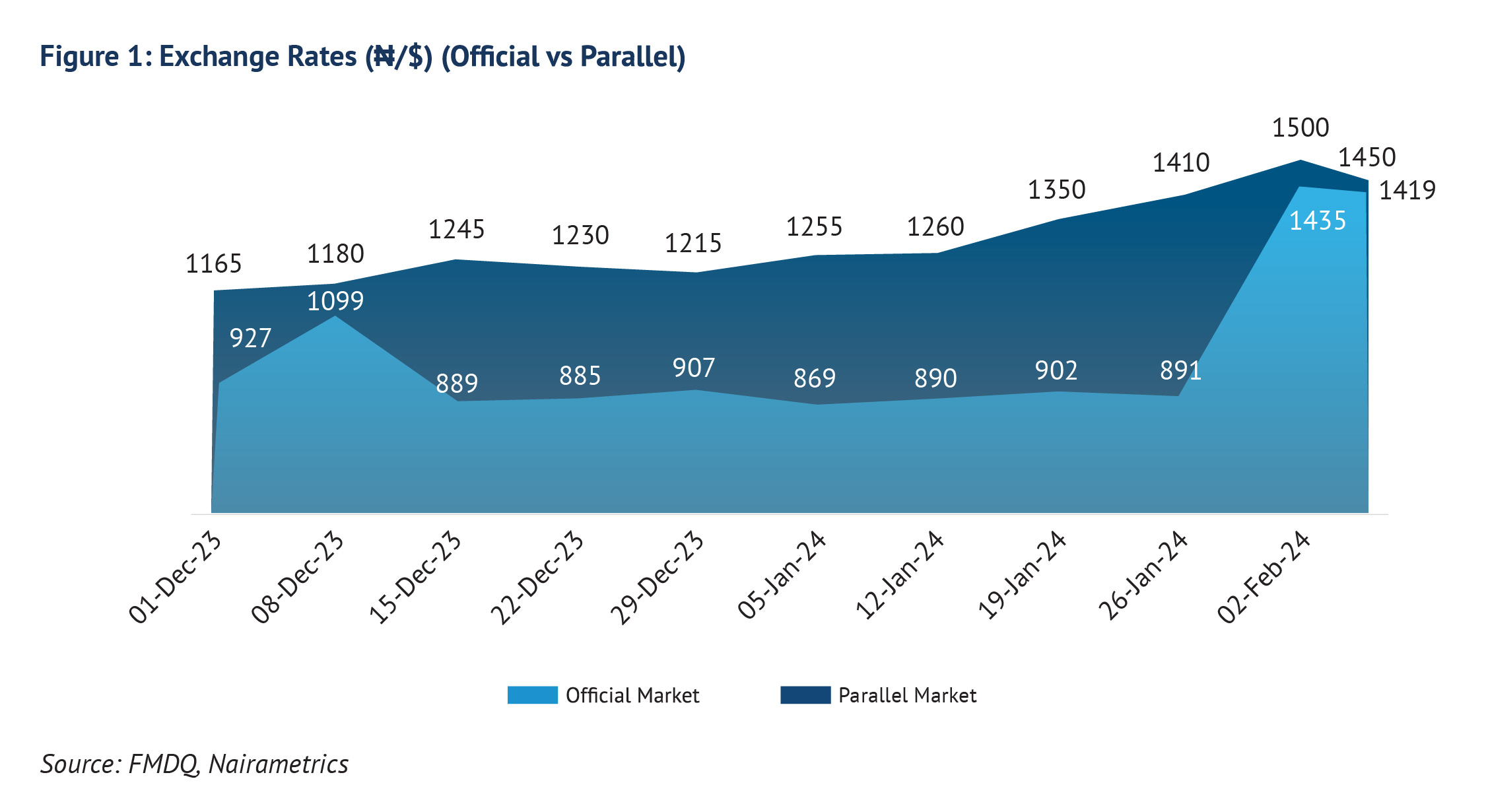

The unfolding narrative on the naira in recent weeks has been nothing short of dramatic. After breaching the ₦1,000 threshold for the first time at the official foreign exchange (FX) market on the 8th of December 2023, the naira went on to lose 37.6% of its value in January 2024 alone, closing the month at ₦1,455.59/$. At the core of Nigeria’s currency conundrum is an external imbalance problem that underpins an FX illiquidity challenge. This has been exacerbated by the distortionary impact of hoarding, stockpiling and panic buying.

In an effort to tackle liquidity challenges, combat market distortions, and promote transparent pricing in the foreign exchange market, the Central Bank of Nigeria (CBN) has swiftly implemented a series of policy measures. These were communicated through a series of circulars, released within a span of three days (January 29th to January 31st, 2024), demonstrating the CBN’s dedication to addressing concerns surrounding the persisting naira weakness.

Figure 1: Exchange Rates (₦/$) (Official vs Parallel)

Rapid Fire Approach

The first circular, released on January 29th, focused on ending underhand practices by reminding authorised dealers to conduct transactions on a ‘willing buyer willing seller’ basis. This directive aimed to eliminate under-reporting of FX transaction rates and ensure transparent pricing. Almost simultaneously, the Financial Market Dealers Quotation (FMDQ) Exchange amended the pricing methodology of foreign exchange transactions, resulting in a ‘price correction’ at the Nigerian Autonomous Foreign Exchange Market (NAFEM), where the naira ended the day at ₦1,413/$, almost at par with the parallel market exchange rate – ₦1,430/$. As at February 6, 2024, the naira traded at ₦1,450/$ at the parallel market, holding a 2% premium over the official market rate of ₦1,450/$.

The second circular, released on January 31, mandated banks to adhere to Net Open Position (NOP) limits, preventing excessive holding of foreign currency assets, something that has allowed banks to profit massively from FX revaluation gains in recent years and upped the incentive to hoard. The new directive stipulates that the NOP must not exceed 20% short or 0% long. Although it is unclear to what extent, it is widely acknowledged that most banks currently have significant long foreign currency positions. Enforcing this guideline will result in the injection of FX liquidity into the market, although it is likely to impinge on profits. At this juncture, it is imperative to acknowledge that the principal justification for numerous savers engaging in hedging activities is the persistent depreciation of the naira, which has rendered business planning unfeasible. The substantial amount of over ₦13 trillion held in domiciliary accounts with banks, which has doubled since 2020, serves as clear evidence of this. What additional measures can the CBN take regarding this situation? Could it consider imposing a cash reserve requirement (CRR) on foreign currency deposits, as is the case in some of its African peers (Ghana and Egypt), and the global giant China? Although we are not explicitly stating that the CBN will follow this approach, it is our belief that implementing such a measure would reduce the appeal of foreign currency deposits and prompt banks to place less emphasis on them.

The third circular targeted International Money Transfer Operators (IMTOs), removing the allowable limit of exchange rates quoted by them as well as limiting their operations to inbound transfers only. This move aims to draw around $22 billion in annual diaspora remittances into the official foreign exchange market as well as enhance the monitoring of international financial transactions. In addition, the CBN now mandates all inbound money transfers to Nigeria to be paid in Naira, further impacting recipients who prefer or require US dollar payouts. The policy could influence remittance channels used by Nigerians abroad and is likely to pose challenges for individuals and businesses accustomed to IMTOs for outbound transfers.

Available data indicates a surge in FX liquidity from $134 million on January 31st to a 19-month high of $844 million on February 5th on the back of these measures that have enabled the naira to trade more freely against the dollar.

Figure 2: FX Turnover (End-January/February 2024) ($’ million)

From Chaos to Clarity

Governor Olayemi Cardoso of the Central Bank of Nigeria (CBN), in a televised speech on February 6, 2024, linked the ongoing volatility in the FX market to inadequate liquidity and provided much-needed clarity on unpaid forex obligations. The CBN inherited $7 billion in unpaid FX commitments, necessitating a forensic investigation by Deloitte to discern between legal and invalid claims. The audit found that $2.4 billion in claims were flawed, including entities that lacked proper import documentation, non-existent entities obtaining allocations, and instances of excessive or unrequested allocations. According to Dr Cardoso, the CBN has cleared $2.3 billion in valid claims, including those from airlines, leaving a balance of $2.2 billion, which it intends to address expeditiously.

We believe that the path to stability and fair value for the naira hinges crucially on clearing the FX backlog, after which FX supply will need to improve for the naira to achieve stability. The CBN’s efforts at improving transparency in the FX market in addition to the near convergence of the official and parallel market exchange rates raise the potential for a recovery of the naira if and when the backlog is cleared. This also lends credence to Governor Cardoso’s description of the naira as “undervalued”. However, the recovery, in the short-term, is premised on a sustained increase in crude oil output (to at least 1.5mbpd), and the receipt of some foreign currency denominated inflows (loans and securitisation of NLNG dividend). Clearly, the CBN is taking steps away from ‘managing’ the currency and towards a market-determined exchange rate. The end game is to restore confidence in the naira and attract investment flows – particularly from remittances (estimated at $22 billion in 2023) and foreign portfolio investments (FPI).

A Return to Orthodoxy

Ahead of the maiden Monetary Policy Committee (MPC) meeting by the CBN’s new leadership, the Governor, once again, has emphasised the return to orthodoxy with a shift to a focus on price stability. The CBN will look to review the effectiveness of the current monetary policy tools and fix the transmission mechanism to ensure the MPC’s decisions are impactful, fulfil their desired objectives and complement the efforts of the fiscal authorities. Some have argued that recent inflationary episodes have been triggered by cost-push phenomena which demand-pull measures proved ineffective in combating, evidenced by the surge in headline inflation in 2022 and 2023 in spite of the cumulative 725 basis point hike in the Monetary Policy Rate (MPR) since May 2022 to 18.75%.

In addition, Dr Cardoso alluded to a revamp of the current communication strategy, with the adoption of a feedback mechanism where the CBN engages with stakeholders on reforms. We believe that these strategic moves adopted in recent weeks lay the groundwork for potential shifts in Nigeria’s monetary policy landscape under Dr. Yemi Cardoso’s leadership. The market is in wait-and-see mode, assessing and seeking further clarity on the long-term impact of these policy changes and their implications for Nigeria’s economic stability.

Looking Ahead – A Delicate Balancing Act

Both theoretical and empirical evidence indicate that it is impossible to tackle the exchange rate issue without first addressing inflation. The Apex bank aims to rein in inflation to 21.4% on the back of its inflation-targeting policy. Annual inflation spiked through 2023 to 28.9% in December – an almost 30-year high – largely due to the naira’s slump, of almost 50%, and the ‘reduction’ of petrol subsidies. We believe that the sharply weaker currency and the recent escalation of conflict in major food-producing areas in the country’s middle-belt raise the risk of another wave of inflationary pressure, which would exacerbate the current cost-of-living crisis.

Cardoso may have answered some questions, but also raised a new one. How will the MPC strike a balance between being cautious about potential increases in the Federal Government’s borrowing costs in 2024 and the necessity of implementing more aggressive policy measures to effectively control inflation, reduce excess liquidity, and raise interest rates to ensure positive returns for long-term savers? This, we believe, will present a major dilemma in the coming months. Dr. Cardoso and his team certainly have their work cut out for them.