History will define 2020 as the “year of the pandemic” and in an interesting feat of hope, 2021 could turn out to be the “year of the vaccine”. The record speed of the entire vaccine process – which includes research, testing, production, approvals and administration – was largely driven by the urgency to curb the apocalyptic effects of the pandemic and could eventually redefine the sciences of vaccines in revolutionary ways.

In Nigeria, despite the obvious weaknesses in data management and testing which would have resulted in lower numbers, the second wave is challenging the resilience of the fragile health system especially in Lagos, the country’s commercial capital and epicentre of the pandemic in the country. In the absence of reliable research to explain the lower than anticipated infection rates in Nigeria and across sub Saharan Africa (ex-South Africa) which many have indolently adduced it to serendipity. Unlike South East Asian states and New Zealand which pursued intentional policies to control the spread of the virus with enviable degrees of success, Nigeria’s better-than-expected fate cannot be linked to a policy framework especially in the face of an unreliable contact tracing system.

We hereby examine some of the major macro themes that will help shape the Nigerian economic landscape in 2021.

The Pandemic & the Vaccine

As much of the world battles the second wave of Covid-19, Nigeria’s numbers have also shown some steady increase to reach new daily highs. In December 2020 alone, Nigeria’s numbers surpassed a threshold of over 1,000 cases daily on five occasions and this has become the norm in the first weeks of 2021. However, Nigeria’s numbers still pale in comparison to much of United States and western European countries which has led to more stringent lockdowns in these countries especially in the latter.

Despite Nigeria’s lower-than-expected numbers, risks still abound in three significant ways. Firstly, Nigeria remains significantly vulnerable to the economic contagion arising from a weak global environment. Secondly, weaknesses in the global macro environment pose significant downsides to the crude oil market which further exposes Nigeria’s vulnerabilities. Thirdly, the discovery of new strains of the virus also portends greater systemic risks to the broader economy and particularly to the health sector as the management of COVID-19 undermines the response to other ailments and the healthcare needs of the populace. Overall, we believe the geopolitical complexities with sourcing the vaccines places Nigeria and the rest of Africa on the backfoot. We believe a mass vaccination program capable of creating herd immunity may not occur in Nigeria in all of 2021. Thus, the country will have to eke out effective ways of managing the spread of the virus and care for affected patients while pursuing measures for the vaccination program.

Interest Rates & Inflation

Nigeria’s average inflation rate has ranged between 11% – 12% over the last two decades, which indicates it is a high-inflationary country. In 2021, we project that inflation will even surpass this long-term average to about 14% – 15% further putting the naira under pressure. Forward guidance from the Central Bank indicates that monetary authorities have an inflation target within the 6% – 9% range. The significant disparity (>600 basis points) between the upper limit of the CBN’s inflation target and the current inflation numbers further reflect the high inflationary trend of the country.

Nigeria’s long-term high inflation is an often overlooked economic indicator with exchange rates enjoying greater prominence in the discourse. This creates a paradox, with Nigeria’s monetary policy strategy unduly focused on the pursuit of a stable currency viewed largely from the prism of foreign exchange and an inertia towards inflation. While Nigerians have long fantasised about a strong currency – often defined as one being at par with major currencies such as the British pound or US dollar – the long term high inflationary trend remains the underbelly of the naira. Agusto & Co. believes Nigeria’s high inflation reflects the country’s weak economic fundamentals and needs to be reined to set the country on the path of long-term prosperity.

Exchange Rate

Outside the management of COVID-19 related disruptions to the economy, the subject of foreign exchange in Nigeria will be the most consequential economic issue in 2021. The pertinent issue will include the management of foreign exchange liquidity. For now, the Central Bank has resorted to its demand management playbook of 2016 which did create a wide spread between the official market and the parallel market at the time. The outcome of the demand management playbook in this COVID era also mirrors that of 2016. The naira is currently trading at an unhealthy arbitrage of N80 to N100 to a dollar between the parallel and the official market as monetary authorities struggle to maintain stability in the foreign exchange market.

The odds against the naira in the foreign exchange market are in two folds. First, there are the long-term fundamental issues. With naira inflation projected to be stubbornly stuck above 15% in 2021 and dollar inflation at a benign 2%, the odds against the naira indicate an inflation rate differential of about 14% between the two currencies. The principle behind the inflation rate differential implies that the erosion in the value of the naira measured by inflation is significantly greater than the dollar. Thus, the 13% inflation differential should result in the naira’s depreciation against the dollar in similar measures. Once again, this reiterates the need to pare back inflation in Nigeria.

The second major issue is the demand-supply dynamics in the foreign exchange market. Nigeria has entered a period of low oil and gas export revenues. In 2021, we project about $30 billion in oil & gas exports, down 20% from about $36 billion in 2020. With net foreign investment also likely to be in negative in 2021 due to the demand management strategy of the Central Bank, there will be significant pressure on reserves and the naira/US dollar exchange rates. With foreign reserves stubbornly stuck below the $40 billion threshold since mid-November 2019, and currently around the $35 billion mark, the CBN has less dry powder to defend the naira at N390/$.

In 2021, the CBN will have to make a big call on devaluation with very little leeway to this decision. The cost of an indecision on this issue in 2016 led to the recession. The 2021 scenario is even more complex as Nigeria is now caught between a rock –the pandemic– and a hard place – the foreign exchange illiquidity – and the cost of indecision this time around will come with greater consequences than in 2016.

On the other end, we note that there are three significant upsides inherent in the unification of the exchange rates in the market. The first of these upsides is that the unification of exchange rates will pare back currency speculation as more high networth investors (HNIs) are divesting from the naira while increasing FCY exposures. Secondly, the currency unification will stimulate investor confidence and shore up foreign direct investment and foreign portfolio investment once again. Nigeria’s FDI position fell to less than a billion dollars in 2020 reaching a decade low as the currency arbitrage hurts investor confidence. Thirdly, businesses operating in the country are subjected to increased operational difficulties owing to the currency situation. As more businesses are unable to meet FCY demands on the official market, they resort to the parallel market and then pass on the higher exchange rate costs to consumers thus stoking inflation.

Despite this grim foreign exchange position, we note that Nigeria is not overleveraged in foreign currency terms especially when compared to other key economies in sub-Saharan African peers. While Nigeria has a foreign currency debt position of 56% to its current account receipts, Kenya and Ghana have positions of over 180% and 70% respectively. However, with local currency debts especially the short-term treasuries being raised at less than 3% – thus leaving investors with over 10% in negative real interest rates – the federal government is quite incentivised to raise more local currency debt than FCY debt. Overall, the big question for followers of the foreign exchange market will be “if the CBN will cave in and devalue the naira in 2021?”.

Nigeria’s Fiscal Position

The federal government has budgeted fiscal spending of about ₦13.6 trillion in 2021. However, Agusto & Co. projects aggregate spending of about ₦10 trillion, while fiscal revenues will be about ₦3.5 trillion, indicating a record deficit of over ₦6 trillion. Despite the worsening fiscal position of the sovereign, the federal government can access credit at lower yields. In addition, the federal government’s increased borrowing from the Central Bank that has risen by more than 500% in five years will likely continue in 2021, thus reducing the dependency of the government on financial markets in a period of higher demand for government securities. With naira yields on government debt securities at about the same levels with dollar yields, the incentives for the carry trade have been effectively nullified, thus making Nigeria an unattractive destination for foreign portfolio investors. Our outlook for 2021 is that real interest rates will remain negative, thus enabling the government to cheaply finance its deficits.

Will the Central Government embark on Macro Reforms in 2021?

Modern day diction is replete with clichés that draw a nexus between crisis and opportunity. Thus, economic historians have always argued that it is much easier to drive macro reforms in periods of downturns than in more prosperous times. This truism is quite valid even amongst a reform sceptical citizenry in a nation like Nigeria. For instance, the current administration has been able to push for Nigeria’s boldest reform in decades in the pricing strategy of petrol riding on the back of the COVID-19 economic downturn by implementing a new pricing plan that seeks to wean the country off the long-term subsidy regime. Reforms have also been enacted in the electricity markets where the government has also allowed price increases to help market operators absorb more costs albeit with some subsidised tariffs for poor consumers.

The COVID induced economic crisis creates a perfect storm to implement market friendly reforms that have long been in the books of this government. We believe the government should expend some of its political capital on a full deregulation of the downstream petroleum industry beyond the current reforms on pricing it has currently implemented. We also believe that the government should seek bolder actions on asset reforms by reducing its exposures to moribund state-owned enterprises such as the refineries. While funds earned from such divestments can then be channelled into other high-impact assets such as critical infrastructure.

Sector Watch – Where are the bright spots?

The pandemic increases global economic risks and the contagion effect of this raises Nigeria’s risk profile in 2021. However, even amidst the slew of risks, opportunities abound.

The telecommunication sector particularly the data segment will continue to show significant upsides in 2021 as work-from-home (WFH) trends continue into the year. We project double digit growth of about 10% in the telecommunications sector GDP in 2021. Beyond, the remote working trend, other growth drivers that will drive the telecommunications sector’s performance include the increased adoption of virtual engagements for business meetings and conferences, schooling, and even social gatherings, in addition to increased social media consumption.

The pandemic has also created an upside in the fintech space as more consumers take to digital payment solutions due to the social distance protocols. We project that in 2021, the value of e-payment transactions will surpass the ₦100 trillion mark thus becoming larger than the country’s GDP. The growth drivers will be the increased adoption of fintech solutions especially on mobile devices.

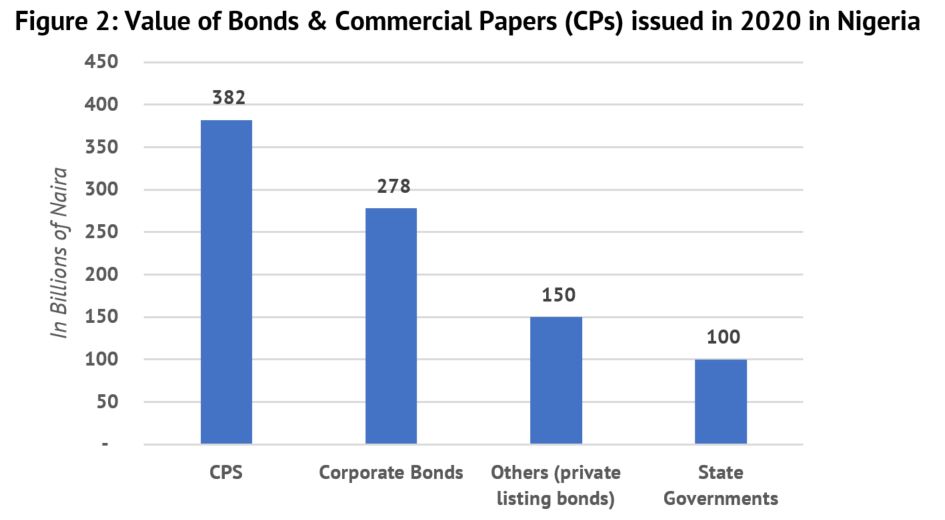

The risk-free yield is a major benchmark for pricing corporate debt instruments. With risk free yields of treasuries currently at low levels of less than 3%, we project significant growth in debt market offerings by corporates at both the short end of the market (in commercial papers) and in long-term maturities via corporate bonds. We believe the corporate debt markets will become more attractive especially for firms that can issue investment grade debt instruments. Overall, we project that over ₦1 trillion will be raised in corporate debt instruments in 2021, representing a 10% increase from the ₦910 billion raised in the prior year (see Figure 2).

The Central Bank’s reforms in the foreign exchange market which now permits recipients of diaspora remittances to access their funds in foreign currency represents the brightest spot in the FX market. We believe this reform policy will increase the competitiveness of the official foreign exchange market against the parallel market.

Winning in 2021

We project a GDP growth of a measly 2% in 2021. A second recession in just five years, a slow post-recession recovery characterised by economic growth (around 2%) that is weaker than the country’s population growth (>2.5%), and the policy inactions to respond to these challenges will test the resilience of many Nigerians in 2021. This portends greater risks for the country that could result in increased social fissures.

The rapid and seismic evolutions in consumer behaviour will prove to be the major driver of corporate performance in this new year. Thus, the winners in 2021 will be those who are able to understand the consumer trends in their industries and make the necessary adjustments to meet the needs or shape consumer behaviour in their favour. For instance, in the FMCG space, the recession leaves consumers poorer and thus there will be a greater demand for products in smaller retail packs. While in the financial sector, weaker spending even by the segment of the middle class and upper class that are still economically buoyant will lead to an increase in savings. This will lead to higher demand for unique investment offerings that can create value for this class of savers. In 2021, we see fintech solutions offering greater competition to the traditional savings products especially amongst the tech savvy millennials.

Overall, the winners in 2021 will be firms and individuals who learn to navigate volatility with greater stability. We believe the year will throw up significant volatility that will require resilience to withstand the shocks and on the other end, foresights to help create paths to success even amidst uncertainty. Nigerians who have long been inured to instability may find their resilience coming under trial this year.